Sometimes managing money is more important than making money

People always talk about making money but no one talks as much about how one should manage their money. Though money management can be an apprehensive subject. One must be aware of their spending, make the right investment decisions along with have a secure plan for their retirement.

So here are 8 money management tips for your better future:

- Keep a track on your spending

Since you have decided to better manage your money you can start by tracking down all your expenses.

Before you make a budget to spend your money see where all your money goes. You can pull up your bank statements, all your bills, your credit as well as debit card statement, this will give you a good reference of all your spending. You can categorize your spending into basic utilities, needs, wants, luxury etc. Based on this you will know what are the areas you spend the most and if they can be pulled back

2. Create a financial Plan and Goal

Creating a short term as well as long term financial goal will give you a clearer picture about how you want your future to look like financially. This will also help you when you set a spending budget for yourself as well as tell you how much and where you need to invest.

3. Make a budget and adhere to it.

Now that you know where you spend your money it will be easy to make a budget. Based on your categories, a lot the required amount to each category based on your wants and need and see where you can cut cost and save up a little each month

4. Pay your monthly bills on time.

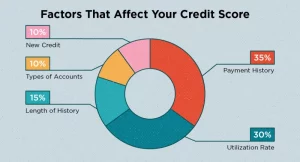

Paying your monthly bills on time is a life skill that has a great impact on your personality. Having a monthly schedule to pay your bills helps you navigate through your budget and know where your basic necessities lie. Paying your monthly bills on time will not only save you with varied late fees but it will also help you improve your CIBIL score.

5. Invest your money wisely and early.

You should start investing your money early on in life so you can grow your money and make more capital in the long term. If investing your money scares you start small don’t jump on big guns initially. Start by 5 % of your monthly income then go to 10%. You can invest your money in stocks or mutual funds, a SIP account or even crypto.

6. Pay all your debts on time

Don’t put yourself in a situation where you are in a pile of debt. People have a habit of taking out loans or use their credit cards excessively with no clear plan or system in place to pay it back. Make sure you pay all your debt on time, it can lower your CIBIL report.

7. Set aside a fund for emergencies

In these unprecedented times you never know when an emergency can happen. There can be a pandemic, due to which you could lose your job or there can be a medical emergency. Situations like these can put you in hot water and take a toll on you mentally emotionally and financially. This is why one should always have a separate stack of funds for times like these so at least when everything else goes south your finances are strong.

8. Have a retirement fund in place

You earn well and live a good life but what about the time when you can’t work but still want to live a good life. Saving up for your retirement should be on a priority list for everyone. So every month set aside a fund for your retirement so you can live a good respectable life when you get old.

Money is a different and tricky subject for everyone. The early on in life you learn how to manage it the early on you will have a healthy relationship with money.